Rethinking Loan Operations: How AI Agents Are Accelerating Approval Cycles

Speed gets all the attention. But the real problem in lending is that no single system owns the workflow from start to finish. That gap is where deals die, and where AI agents are making the most meaningful difference.

Key Takeaways

- Loan processing delays are caused by workflow fragmentation, not just processing speed.

- Around 68% of online loan applications are abandoned, most often due to friction and slow responses.

- RPA reaches a hard ceiling in lending because it handles tasks, not decisions or exceptions.

- Agentic AI introduces a third capability layer: end-to-end workflow orchestration with contextual reasoning.

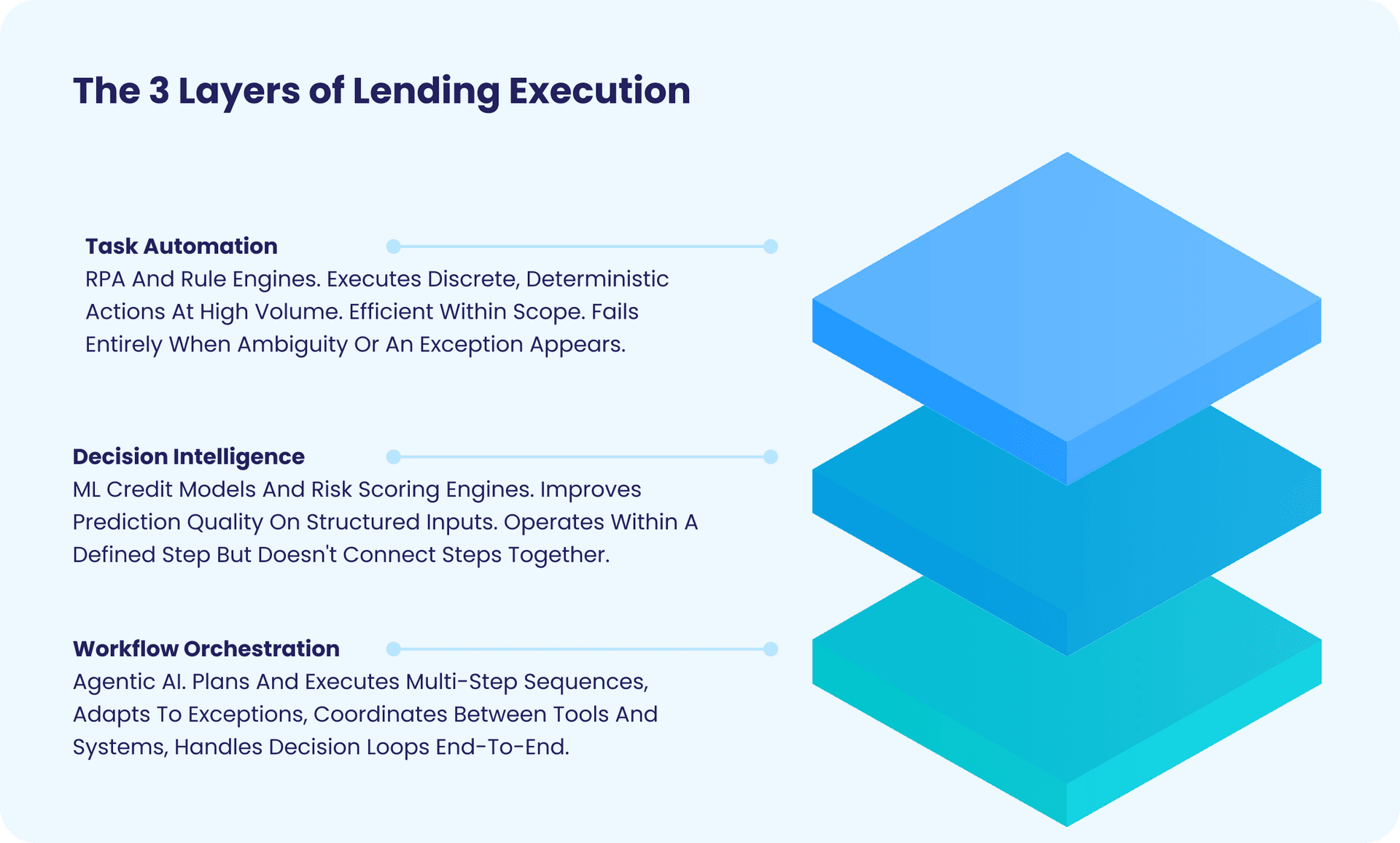

- The 3 Layers of Lending Execution framework distinguishes task automation, decision intelligence, and workflow orchestration.

- xLoop's agentic architecture includes 12 interconnected layers, from guardrails to observability, built for regulated lending environments.

- Explainability and fair lending compliance are structural features of well-designed agentic systems, not retrofits.

The Lending Bottleneck Isn't Speed. It's Fragmentation.

Here's a situation most lending leaders will recognise instantly.

A qualified borrower submits an application on Monday. Their documents are complete. Their credit profile is solid. And yet by Thursday, the application is still sitting in a queue, waiting on a bureau pull that needs to be manually triggered, a document that needs to be re-uploaded in a different format, and a risk officer who is handling three other files.

The team isn't slow. The problem is structural. A single loan application touches five or six different systems, crosses at least three teams, and gets handed off through email threads and spreadsheet trackers that nobody designed for this volume.

That fragmentation is the actual bottleneck. Solve it, and the speed problem largely resolves itself. This is exactly the premise behind modern AI agents for loan processing, and why they represent something genuinely different from the automation tools that came before them.

The Lending Speed Gap: Why Customers Are Walking Away

The competitive pressure is no longer something banks can afford to monitor from a distance. Fintech lenders are approving personal loans in minutes. SME credit lines are being extended within hours on fully digital stacks. Traditional banks and NBFCs, constrained by legacy infrastructure and siloed workflows, are still measuring the same processes in days.

68%

of online loan applications are abandoned before completion

source: MortgagePoint, 2025

70%

of banks have lost clients directly due to slow onboarding and processing

source: Fenergo, 2025

48%

of borrowers who experience digital friction take their business elsewhere

source: MortgagePoint, 2025

What makes this especially costly is the compounding effect. A lender that loses 68% of its applicants to abandonment isn't just losing origination revenue on those specific loans. It's losing the relationship. That borrower goes to a fintech, gets approved in minutes, and has little reason to return.

TransUnion's Q1 2025 Credit Industry Insights Report puts a sharper point on this: fintech firms now account for nearly 50% of new personal loan account balances, up significantly from just a few years ago. That market share didn't materialise because fintechs have better risk models. It happened because they made the process easier and faster.

A 2024 McKinsey report found that 60% of borrowers rank fast approval and disbursal as the single most important factor when choosing a lender, above interest rate and above brand reputation. The institutions winning on conversion right now are offering faster certainty. For a borrower with options, certainty is the product.

The Automation Ceiling: Why RPA Plateaus In Lending

Most lending operations that tried to solve this problem over the last decade reached for Robotic Process Automation. And for a period, it worked.

RPA automated the rules-based tasks that were eating underwriter time: pulling credit scores, routing documents between systems, populating templates, triggering notifications. Real productivity gains. Real cost savings. Institutions that deployed RPA well reduced processing time and freed up capacity.

But then something predictable happened. The gains stopped.

RPA is a task execution layer. It follows deterministic rules: if field A equals value B, perform action C. It cannot interpret ambiguity, adapt to unexpected document formats, reason about incomplete information, or make contextual judgments. And lending workflows are saturated with exactly those requirements.

Think about what happens in practice. A self-employed applicant submits three months of bank statements in a format the system doesn't recognise. RPA stops. A co-applicant introduces a regulatory edge case that the rule engine wasn't configured for. RPA stops. An income figure doesn't reconcile with declared liabilities. RPA stops, and a human steps in to resolve it.

In most RPA-enabled lending operations, that human exception handling still covers 25 to 40 percent of all applications. That's selective automation, with all the overhead that implies. The hardest parts of lending, the judgment, the interpretation, the exception management, were never automated at all.

McKinsey's analysis on modernising loan operations frames this precisely: even banks that made significant automation investments are 40% less productive than digital-native lenders, primarily because of organisational silos and the inability to manage exceptions at scale. The ceiling is structural, and it has nothing to do with the quality of the RPA implementation.

From Tasks To Workflows: The Rise Of Agentic AI

The meaningful shift in lending automation is workflow ownership: the ability for a system to manage a sequence of decisions end-to-end rather than executing isolated tasks and handing off.

To understand what that actually means in a lending context, it helps to think about execution in three distinct layers.

The 3 Layers of Lending Execution

Most institutions that have invested in AI in lending have built capability at Layers 1 and 2. They've automated data extraction. They've deployed ML credit models. What they haven't done is connect those capabilities into a single, orchestrated workflow that can manage itself from application intake to offer generation.

An AI agent manages a sequence of tasks, monitors outputs at each step, handles deviations when they arise, calls the right tools at the right moment, and closes loops that previously required human coordination. The result is continuous processing, without the handoff failures between teams and systems that create delays in the first place.

Benchmarking The Shift: Manual Vs RPA Vs Agentic AI

Speed comparisons are the obvious starting point, but they're an incomplete measure of the transformation. What matters operationally is performance across the full set of dimensions that determine cost, risk, and scale in a lending business.

| Dimension | Manual Processing | RPA-Enabled | Agentic AI |

|---|---|---|---|

| End-to-end cycle time | 5 to 15 days | 2 to 5 days | Hours to 1 day |

| Exception handling | Human review for all edge cases | Stops and escalates to human | Contextual resolution with full audit trail |

| Workflow ownership | Distributed across teams | Partial. Breaks at decision points. | End-to-end orchestration |

| Incomplete application handling | Manual follow-up queues | Rule-triggered nudges only | Proactive gap identification and resolution |

| Compliance documentation | Manual and inconsistent | Structured logging of automated steps | Full reasoning trace per decision |

| Scalability | Linear with headcount | Moderate. Breaks under format variation. | Near-linear volume scaling |

| Credit model integration | Analysts pull scores manually | Automated score retrieval | Dynamic synthesis of bureau and alternative data |

| Cost per application | High (labour-intensive) | Moderate (labour at exception points) | Low and declining at scale |

| Fair lending auditability | Difficult. Human reasoning unlogged. | Partial. Rule logic documented. | Structured explanations per decision |

The pattern is consistent across every dimension. RPA closes part of the gap between manual and optimised, but it leaves the hardest operational challenges largely unaddressed. Agentic AI addresses all of them within the same deployment.

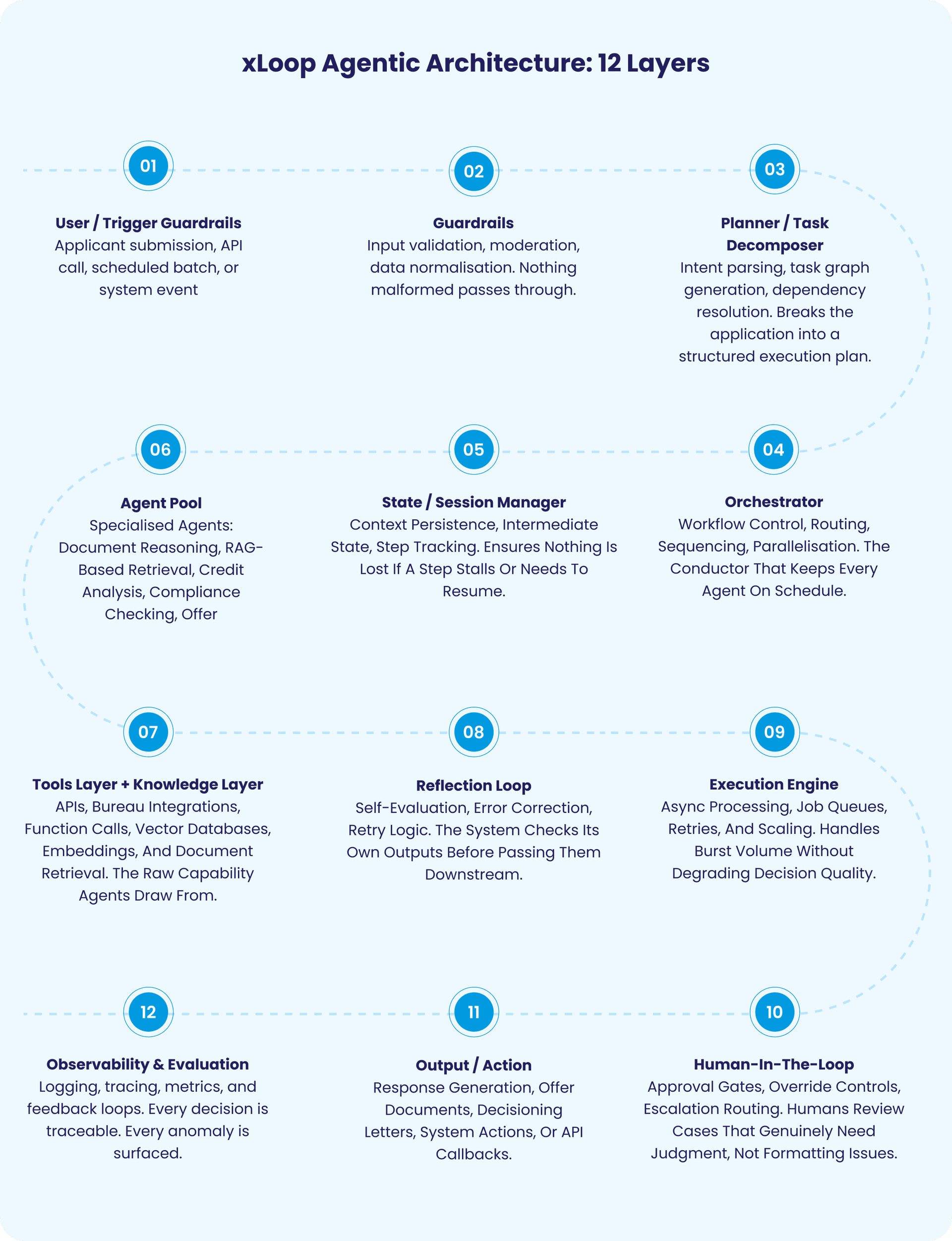

How The XLoop Agentic Architecture Actually Works

A production-grade agentic AI system for lending is a layered architecture of specialised components, each with a defined role, working in concert across the full application lifecycle. Here's how we’ve structured this for lending environments.

A few things are worth highlighting about this architecture specifically.

The Reflection Loop at Layer 8 is not a standard feature in most automation systems. It means the agent evaluates its own output before surfacing it. If a document extraction result has low confidence, the agent flags it internally and attempts an alternative approach before escalating to a human. This alone eliminates a large proportion of avoidable human touchpoints.

The State Manager at Layer 5 is what allows the system to handle interrupted workflows without losing context. If an applicant drops off mid-application and returns three days later, the system resumes exactly where it left off, with all prior context intact. For a borrower on mobile at 11pm, that resumability is what keeps the application alive.

And the Human-in-the-Loop at Layer 10 is designed deliberately, not as a failsafe, but as a governance feature. The system routes to a human when the application genuinely requires it. The human receives a structured brief with all relevant context pre-assembled, rather than reconstructing the picture from raw system logs.

Smarter Credit Decisioning: How AI Agents Go Beyond The Bureau Score

Traditional credit models work well for applicants with clean, established credit histories. They're systematically limited for everyone else. A self-employed business owner with irregular payroll but strong cash flow. A first-time borrower with no bureau history but consistent rent payments and utility bills. A small manufacturer whose GST filings tell a very different story than their declared income.

McKinsey's AI-powered decisioning research notes that traditional bureau-based models fail a large segment of consumers and SMEs who lack formal credit histories, pushing them toward non-bank credit sources. Many of these applicants are creditworthy. The bureau model simply lacks the signals to assess them accurately.

AI agents in the credit decisioning layer address this by expanding the input set and reasoning across it contextually.

- Bureau data: primary tradeline history, delinquency records, inquiry patterns

- Bank statement analysis: income regularity, cash flow volatility, recurring obligations, balance trends

- GST returns and MCA filings: for MSME lending, a more reliable signal than many lenders realise

- UPI and payment network data: transaction frequency and counterparty patterns

- Property or asset registry: for secured products, collateral valuation and encumbrance status

The agent weighs these signals contextually, adjusting their relative importance based on the applicant's profile and the specific product being underwritten. That reasoning is the part that produces better decisions and better auditability at the same time.

Upstart's AI model, which analyses over 1,600 data points per applicant including education history, employment patterns, and financial behaviour, has consistently approved creditworthy borrowers who would have been rejected under traditional scoring. That's the practical case for alternative data in action.

Handling Edge Cases In Real Lending Environments

The clean application is not the hard problem. It never was. The hard problem is everything else.

Co-applicants with documents in different formats. Businesses mid-restructuring with inconsistent filing histories. Applicants with income across multiple currencies. NRI borrowers whose overseas income is documented in a format the LOS doesn't recognise. Collateral values tied to disputed registries.

These aren't rare exceptions. In a portfolio of any meaningful size, they're a constant. And the way a lending system handles them determines whether it's genuinely scalable or just performant under ideal conditions.

In the xLoop architecture, the Orchestrator maintains a growing library of exception patterns and resolution strategies. When the document agent surfaces an anomaly, say a mismatch between a PAN name and the name on submitted bank statements, the Orchestrator doesn't freeze. It checks whether the discrepancy matches a known pattern, applies the appropriate resolution logic, logs the decision with its rationale, and continues processing.

If the anomaly is genuinely novel, the system generates a structured escalation package for human review. Not a bare flag in a queue. A complete brief: the documents involved, the discrepancy identified, the resolution options available, and the recommended path. The human makes a decision in minutes rather than reconstructing the context from scratch.

This is what genuine scalability looks like in lending: complexity handled at volume, without a proportional increase in human hours.

Compliance, Explainability, And Fair Lending

Regulatory concern is the most legitimate reason lending leaders slow down AI adoption. And it deserves precise answers, not reassurances.

The challenge with opaque credit models has always been the same: they make good predictions but they can't explain themselves. That's a problem for adverse action notices, for fair lending audits, and for any examiner who asks why a particular applicant was declined.

Agentic AI systems, when properly designed, solve this structurally. Every step in the reasoning chain is logged: which data sources were consulted, what values were extracted, which rules were applied, and what the output was. This audit trail is generated as a byproduct of normal operation, not assembled retrospectively when a regulator asks for it.

- Adverse action documentation: Because the decision trail is structured and complete, adverse action notices can be populated programmatically from the system's own reasoning log, consistently and accurately across every declined application.

- Bias monitoring: Decision outputs can be analysed across demographic segments to identify differential impact patterns. Agentic systems make this tractable because the data is structured from the start, not reconstructed after the fact.

- Audit readiness: Regulatory examinations require lenders to demonstrate consistent, documented decision processes. Fenergo's 2025 report notes that AML fines alone reached $4.6 billion globally in 2024 The cost of inadequate documentation is not abstract.

The compliance advantage here over both manual processing and RPA is that the reasoning is structured and complete across the full workflow. Human decisions are often reasonable but poorly documented. RPA decisions are documented but narrow. Agentic decisions are documented, contextual, and auditable end-to-end.

Metrics That Actually Matter In AI-Led Lending

Most ROI calculations for lending automation start and end with cycle time and cost per application. Those metrics matter, but they're incomplete. The institutions that sustainably outperform on lending operations are tracking a different set of indicators.

Exception rate reduction

60 to 75%

Exception rate reduction Fewer applications requiring human intervention in mature agentic deployments versus RPA Application completion rate

Up 20 to 35%

Proactive gap identification recovers abandonments before they occur. Decision consistency

Near 100%

Identical inputs produce identical outputs. Critical for fair lending and audit defence. Audit preparation time

Down 80%+

Structured decision trails replace manual documentation reconstruction during regulatory reviews

Institutions should also track their straight-through processing rate: the proportion of applications completed end-to-end without any human touchpoint. In well-tuned agentic deployments, this rate scales with system maturity. Starting at 40 to 50 percent in initial deployment and reaching 70 to 80 percent within six to twelve months is a realistic trajectory for most retail lending portfolios.

That trajectory matters because the system improves as it processes more applications. The exception library grows. The resolution logic becomes more precise. The model gets better at flagging the cases that genuinely need a human versus the ones it can handle independently. This is a characteristic of agentic systems specifically, and one that RPA and static credit models cannot replicate.

xLoop's Approach To Deploying Agentic AI In Lending

A few things distinguish how we approach this, beyond the architecture itself.

1. Workflow-First, Not Feature-First

The design process starts with the full end-to-end lending workflow, not individual automation use cases. Agent handoffs, exception paths, escalation logic, and state management are built into the architecture from day one. Bolt-on automation is where most deployments fail: they automate individual steps well and then create new bottlenecks at the transitions between them.

2. Configurable By Lending Context

A personal loan origination workflow is structurally different from an SME working capital facility or a mortgage application. xLoop's agent configurations are parameterised by product type, regulatory jurisdiction, and data availability, so the same underlying architecture serves multiple lending contexts without being rebuilt from scratch for each one.

3. Human-In-The-Loop By Design

The goal is not to remove humans from lending decisions. It's to ensure that when humans are involved, they're reviewing cases that genuinely need judgment, with all relevant context already assembled. xLoop's tiered review model distinguishes between applications that should be fully automated, applications that should be auto-decided but reviewed post-hoc, and applications that require pre-decision input. Institutions calibrate this based on their own risk appetite and regulatory context.

4. Observability From Day One

Layer 12 of the architecture, the Observability and Evaluation layer, is active from the first application processed. Every decision is traceable. Every anomaly is surfaced. Every feedback signal feeds back into model evaluation. This is what makes the system improvable over time and defensible under regulatory scrutiny.

Assess Your Lending Operations Maturity with xLoop

Understand where your loan processing stands and where AI agents can drive the biggest impact

FAQs

Frequently Asked Questions

Table of Contents

Newsletter Signup

Tomorrow's Tech & Leadership Insights in

Your Inbox

Discover New Ideas

Agentic AI in Wealth Management: Building Self-Optimising Investment Portfolios

AI Document Processing ROI: How Mid-Market Companies Are Cutting Processing Time by 60% (And What It Costs to Wait)

Is Your AI Actually Secure? What Enterprise Leaders Need to Know in 2026

Knowledge Hub